By bne IntelliNews May 18, 2020

Russia’s federal budget posted a surplus of 0.2% of GDP in April 2020, and surpluses of 0.5% in 1Q20 and 0.4% in 4M20, according to the latest data from the Finance Ministry.

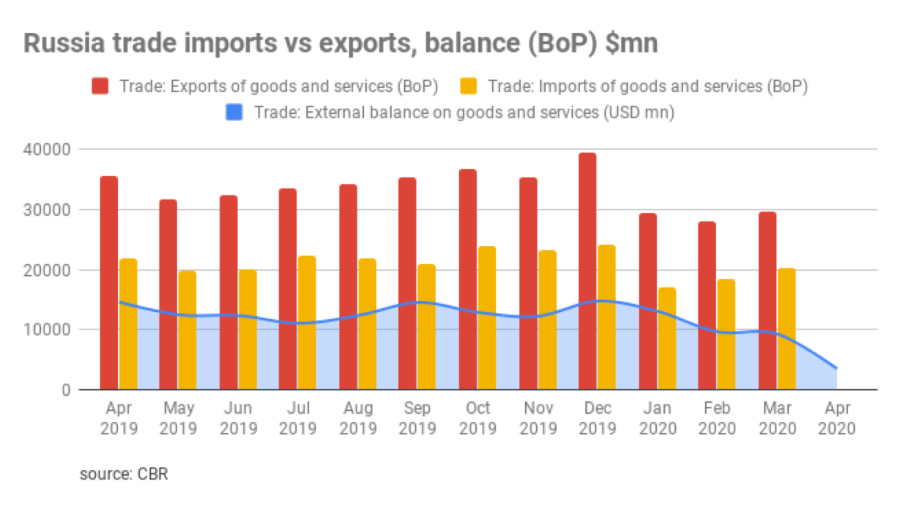

At the same time, Russian maintained a double external surplus, with the trade balance posting a surplus of $3.5bn ($35.6bn in 4M20) and current account also in surplus of $1.8bn ($23.5bn in 4M20), according to the Central Bank of Russia (CBR) data.

As reported by bne IntelliNews, its solid fiscal and external position is the backbone of Russia’s investment case, especially in this period of global volatility.

Prudent fiscal response

“Contrary to the global trend of rapidly growing budget deficits and public debt, Russia maintained a surplus budget last month – even despite a massive drop in the crude [oil] price (-38% month on month),” chief economist of BCS Global Markets Vladimir Tikhomirov commented on May 17.

BCS GM estimates a 49% increase in budget expenditures in April versus 1Q20 in seasonally adjusted terms, but this was almost fully compensated by a 46% rise in revenue. While revenues from oil and gas have dropped by 26% m/m, non-oil revenues posted a major increase of 89%.

Notably, the National Welfare Fund (NWF) showed no significant change in its volume as of May 1 amounting to $170.6bn.

“The only notable change in the NWF was a decline in the volume of its liquid assets from 9.8% to 7.4% of GDP, but that was due to the transfer on the balance of the fund of Sberbank shares that the government has purchased from the CBR,” said BCS GM.

Still, Tikhomirov expects the federal budget to be closed with a deficit in May; however, this is likely to be covered through issuance of new public debt (OFZs) rather than by withdrawals from NWF.

As reported by bne IntelliNews, Russia’s economic stimulus response to coronavirus (COVID-19) has been seen as rather moderate and prioritising the prudent fiscal position. This, in part, has allowed the CBR to cut the interest rates, and to maintain Russia’s investment ratings, but risks greater fallout in the case of a prolonged epidemic.

This month Finance Minister Anton Siluanov said a base-case scenario for the recession in 2020 is 5% GDP contraction, while the government could borrow 1.5-2% of GDP (RUB4-4.5 trillion, or $53bn-60bn) in 2020 to finance the 4% budget deficit.

No capital exodus

On the external finances side, the trade surplus remained resilient despite the 75% year-on-year decline in the price of Urals oil. The current account surplus was supported by a modest volume of capital outflows.

“The latter reached $6.9bn in April ($23.9bn in 4M20) – a far cry from the monthly outflows of between $20bn and $50bn that Russia recorded in late 2008 and early 2014,” Tikhomirov wrote, noting that Russia has managed to escape significant deterioration in its balance of payments – certainly see as “a major positive”.

“Foreign investors continue to view Russian bonds and equities as safe investments, which explains why we have not seen a massive exodus of foreign money from the local stock market,” the BCS GM economist believes.

BCS GM forecasts that in 2020 Russia’s foreign trade surplus will reach $102bn, while its current account will be closed with a surplus of $45bn. Both estimates are much more bullish than those of the CBR ($43bn and $35bn respectively).